Stationarity tests

1 Dickey–Fuller test

The Dickey–Fuller test tests the null hypothesis that a unit root is present in an autoregressive (AR) model. The alternative hypothesis is different depending on which version of the test is used, but is usually stationarity or trend-stationarity. Let’s consider an AR(1) model, i.e.

The, the Dickey–Fuller hypothesis are:

2 Augmented Dickey–Fuller test

The augmented Dickey–Fuller is a more general version of the Dickey–Fuller test for a general AR(p) model, i.e.

Then, the augmented Dickey–Fuller hypothesis are:

3 Kolmogorov-Smirnov test

The Kolmogorov–Smirnov two-sample test (KS test) can be used to test whether two samples came from the same distribution. Let’s define the empirical distribution function

To apply the test in a time series settings, it is possible to random split the original series in two sub samples and apply the test above.

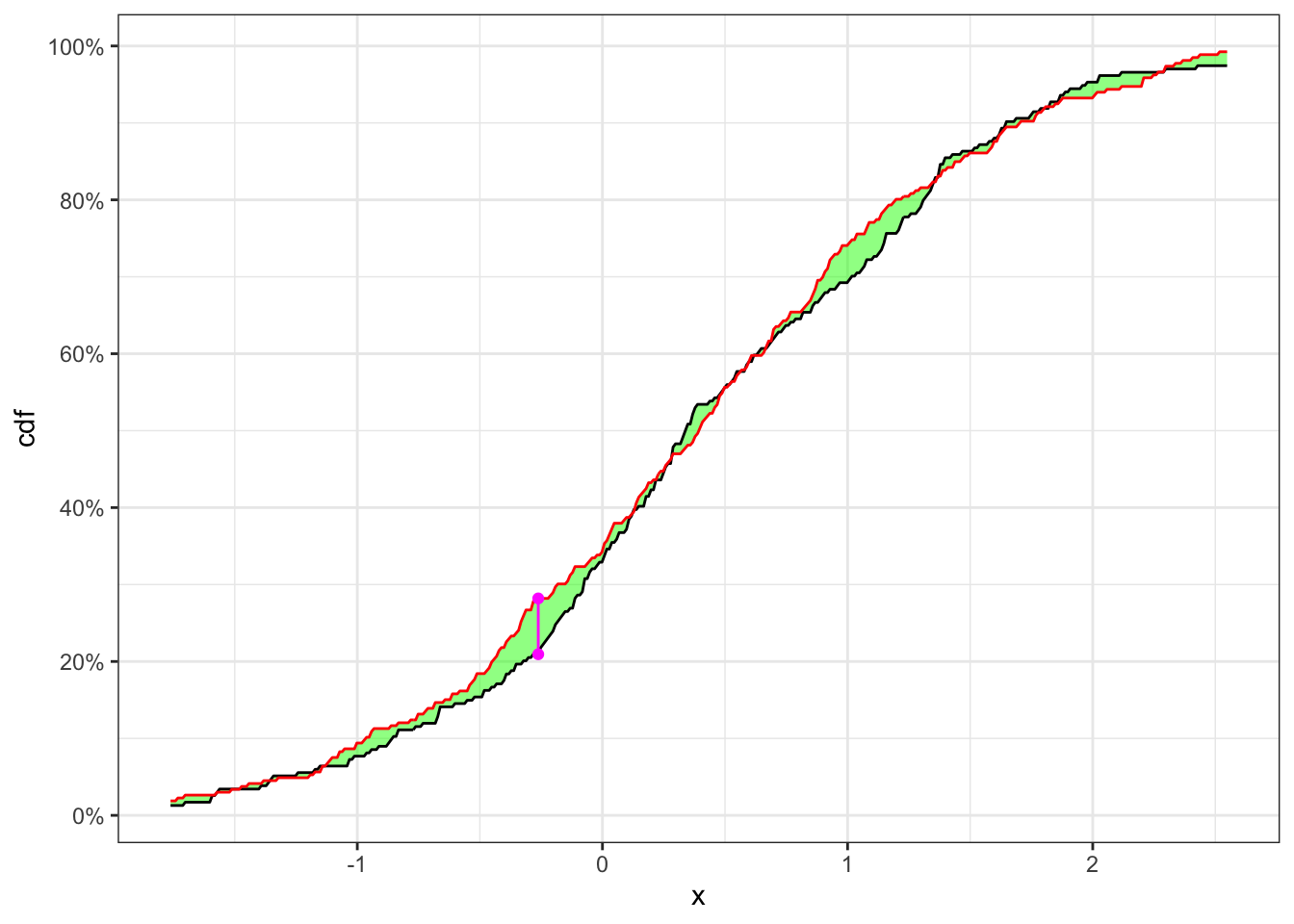

3.1 Example: check stationary

Let’s simulate 500 observations of

KS-test on a stationary time series

# ============== Setups ==============

set.seed(5) # random seed

ci <- 0.05 # confidence level (alpha)

n <- 500 # number of simulations

# ====================================

# Simulated stationary sample

x <- rnorm(n, 0.4, 1)

# Random split of the time series

idx_split <- sample(n, 1)

x1 <- x[1:idx_split]

x2 <- x[(idx_split+1):n]

# Number of elements for each sub sample

n1 <- length(x1)

n2 <- length(x2)

# Grid of values for KS-statistic

grid <- seq(quantile(x, 0.015), quantile(x, 0.985), 0.01)

# Empiric cdfs

cdf_1 <- ecdf(x1)

cdf_2 <- ecdf(x2)

# KS-statistic

ks_stat <- max(abs(cdf_1(grid) - cdf_2(grid)))

# Rejection level with probability alpha

rejection_lev <- sqrt(-0.5*log(ci/2))*sqrt((n1+n2)/(n1*n2))

# ========================== Plot ==========================

y_breaks <- seq(0, 1, 0.2)

y_labels <- paste0(format(y_breaks*100, digits = 2), "%")

grid_max <- grid[which.max(abs(cdf_1(grid) - cdf_2(grid)))]

ggplot()+

geom_ribbon(aes(grid, ymax = cdf_1(grid), ymin = cdf_2(grid)),

alpha = 0.5, fill = "green") +

geom_line(aes(grid, cdf_1(grid)))+

geom_line(aes(grid, cdf_2(grid)), color = "red")+

geom_segment(aes(x = grid_max, xend = grid_max,

y = cdf_1(grid_max), yend = cdf_2(grid_max)),

linetype = "solid", color = "magenta")+

geom_point(aes(grid_max, cdf_1(grid_max)), color = "magenta")+

geom_point(aes(grid_max, cdf_2(grid_max)), color = "magenta")+

scale_y_continuous(breaks = y_breaks, labels = y_labels)+

labs(x = "x", y = "cdf")+

theme_bw()

In Table 1 the null hypothesis, i.e. the two samples come from the same distribution, is not reject with the confidence level

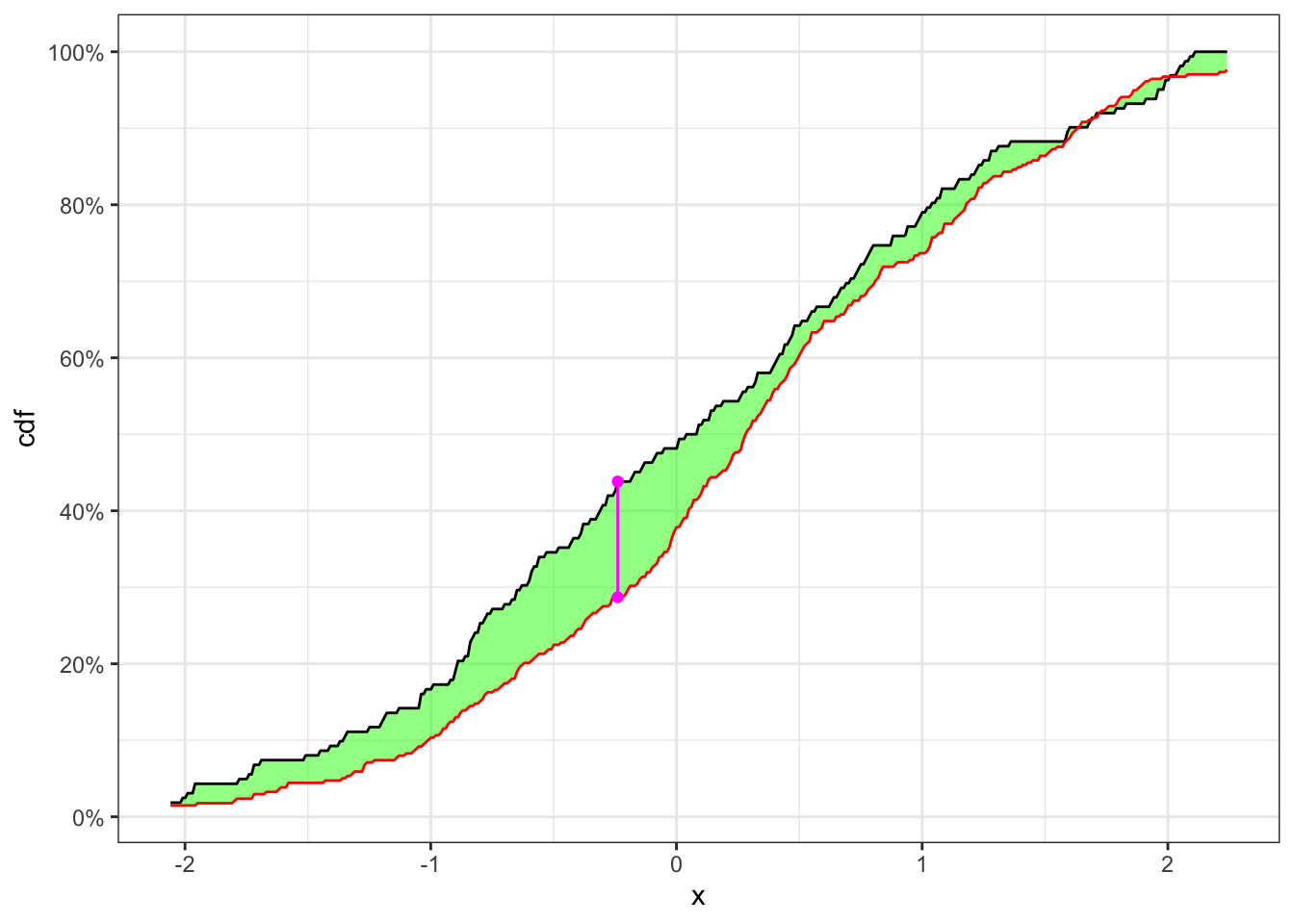

3.2 Example: check non-stationary

Let’s now simulate 250 observations as

KS-test on a non-stationary time series

# ============== Setups ==============

set.seed(2) # random seed

ci <- 0.05 # confidence level (alpha)

n <- 500 # number of simulations

# ====================================

# Simulated non-stationary sample

x1 <- rnorm(n/2, 0, 1)

x2 <- rnorm(n/2, 0.3, 1)

x <- c(x1, x2)

# Random split of the time series

idx_split <- sample(n, 1)

x1 <- x[1:idx_split]

x2 <- x[(idx_split+1):n]

# Number of elements for each sub sample

n1 <- length(x1)

n2 <- length(x2)

# Grid of values for KS-statistic

grid <- seq(quantile(x, 0.015), quantile(x, 0.985), 0.01)

# Empiric cdfs

cdf_1 <- ecdf(x1)

cdf_2 <- ecdf(x2)

# KS-statistic

ks_stat <- max(abs(cdf_1(grid) - cdf_2(grid)))

# Rejection level

rejection_lev <- sqrt(-0.5*log(ci/2))*sqrt((n1+n2)/(n1*n2))

# ========================== Plot ==========================

y_breaks <- seq(0, 1, 0.2)

y_labels <- paste0(format(y_breaks*100, digits = 2), "%")

grid_max <- grid[which.max(abs(cdf_1(grid) - cdf_2(grid)))]

ggplot()+

geom_ribbon(aes(grid, ymax = cdf_1(grid), ymin = cdf_2(grid)),

alpha = 0.5, fill = "green") +

geom_line(aes(grid, cdf_1(grid)))+

geom_line(aes(grid, cdf_2(grid)), color = "red")+

geom_segment(aes(x = grid_max, xend = grid_max,

y = cdf_1(grid_max), yend = cdf_2(grid_max)),

linetype = "solid", color = "magenta")+

geom_point(aes(grid_max, cdf_1(grid_max)), color = "magenta")+

geom_point(aes(grid_max, cdf_2(grid_max)), color = "magenta")+

scale_y_continuous(breaks = y_breaks, labels = y_labels)+

labs(x = "x", y = "cdf")+

theme_bw()

In Table 2 the null hypothesis, i.e. the two samples come from the same distribution, is reject with a confidence level

Citation

@online{sartini2024,

author = {Sartini, Beniamino},

title = {Stationarity Tests},

date = {2024-05-01},

url = {https://greenfin.it/statistics/tests/stationarity-tests.html},

langid = {en}

}