ARMA process

1 MA(q) process

In time series analysis, the moving-average process (MA) denotes a model for univariate time series. For a general order \(q\) it is defined as a process \(X_t \sim MA(q)\) when: \[ x_t = \mu + \sum_{i=1}^{q}\theta_i u_{t-i} + u_{t} \text{.} \] To be very general the error term is \(u_t \sim \text{MDS}(0,\sigma^2)\) is as ergotic \(\text{MDS}\), i.e. martingale difference sequence.

Let’s consider a process \(X_t \sim MA(1)\), i.e. \[ x_t = \mu + \theta_1 u_{t-1} + u_{t} \text{.} \] Independently from the distribution of \(u_t\), the long term expectation of the process is computed as \[ \mathbb{E}\{X_t\} = \mu + \mathbb{E}\{u_{t}\} + \theta_1 \mathbb{E}\{u_{t-1}\} = \mu \text{.} \] The variance instead, \[ \begin{aligned} \gamma_0 {} & = \mathbb{V}\{X_t\} = \\ & = \mathbb{V}\{u_{t}\} + \theta_1^2 \mathbb{V}\{u_{t-1}\} = \\ & = \sigma^2 + \theta_{1} \sigma^2 = \\ & = \sigma^2(1+\theta_{1}^2) \end{aligned} \] and, in general, the auto covariance function is defined as \[ \begin{aligned} \gamma_1 {} & = \mathbb{C}v\{X_t, X_{t-1}\} = \\ & = \mathbb{E}\{(u_{t} + \theta_{1}u_{t-1} )(u_{t-1} + \theta_{1}u_{t-2})\} = \\ & = \theta_{1} \mathbb{V}\{u_{t-1}\} = \\ & = \theta_{1} \sigma^2 \end{aligned} \] It follows that, the auto covariance function is bounded up to the first lag, i.e. \[ \begin{aligned} \sum_{j = 0}^{\infty} |\gamma_{j}| {} & = \gamma_{0} + \gamma_{1} + 0 + 0 + \dots = \\ & = \sigma^2 (1 + \theta_{1} + \theta_{1}^2) \end{aligned} \] Finally, the correlation between two lags is defined as: \[ \begin{aligned} \rho_{1} {} & = \mathbb{C}r\{X_t, X_{t-1}\} = \\ & = \frac{\mathbb{C}v\{X_t, X_{t-1}\}}{\sqrt{\mathbb{V}\{X_t\} \mathbb{V}\{X_{t-1}\}}} = \\ & = \frac{\gamma_1}{\gamma_0} = \frac{\theta_{1}}{1 + \theta_{1}^2} \text{.} \end{aligned} \] It follows that the process is always stationary independently from the parameter \(\theta_1\).

1.1 Example: MA(1)

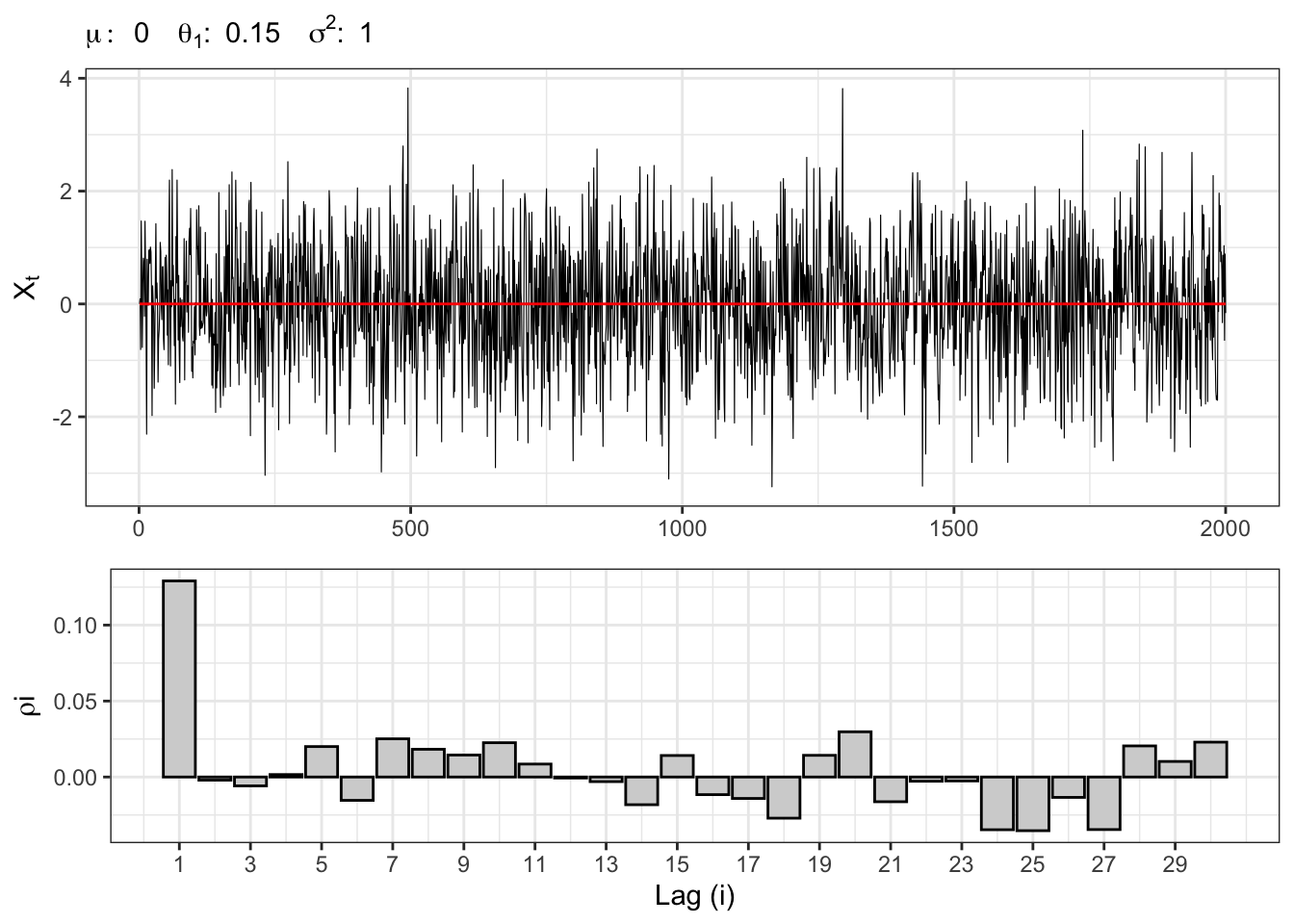

Let’s simulate a moving-average Gaussian process \(X_t \sim MA(1)\), i.e. \[ x_t = \mu + \theta_1 u_{t-1} + u_{t} \text{,} \] where \(u_t \sim \mathcal{N}(0, \sigma^2)\).

MA(1) simulation

# ==================== Setups =====================

set.seed(1) # random seed

t_bar <- 2000 # number of simulations

par <- c(mu = 0, theta1 = 0.15) # parameters

sigma <- 1 # std. deviation residuals

lag.max <- 30 # maximum lag for ACF plot

Xt <- c(par[1]) # starting point

# ================== Simulation ===================

# Simulated residuals

eps <- rnorm(t_bar, mean=0, sd=sigma)

# Simulated MA(1)

for(t in 2:t_bar){

Xt[t] <- par[1] + par[2]*eps[t-1] + eps[t]

}

# ===================== Plot ======================

# MA(1) simulation process

plot_ma <- ggplot()+

geom_line(aes(1:t_bar, Xt), size = 0.2)+

geom_line(aes(1:t_bar, par[1]), color = "red")+

theme_bw()+

labs(x = NULL, y = TeX("$X_t$"),

subtitle = TeX(paste0("$\\mu:\\;", par[1],

"\\;\\; \\theta_{1}:\\;", par[2],

"\\;\\; \\sigma^2 : \\;", sigma^2,

"$")))

# MA(1) autocorrelation

lags <- 1:lag.max

x_breaks <- seq(1, lag.max, 2)

acf_j <- acf(Xt, plot = FALSE, lag.max = lag.max, type = "correlation")$acf[,,1][-1]

plot_acf <- ggplot()+

geom_histogram(aes(lags, acf_j), stat = "identity",

color = "black", fill = "lightgray")+

scale_x_continuous(breaks = x_breaks, labels = x_breaks)+

labs(x = "Lag (i)", y = TeX("$\\rho{i}$"))+

theme_bw()

gridExtra::grid.arrange(plot_ma, plot_acf, heights = c(0.6, 0.4))

Table code

kab <- bind_rows(

tibble(Statistic = "$$\\mathbb{E}\\{X_t\\}$$",

Theoric = par[1],

Empiric = mean(Xt)),

tibble(Statistic = "$$\\mathbb{V}\\{X_t\\}$$",

Theoric = sigma^2 * (1 + par[2]^2),

Empiric = var(Xt)),

tibble(Statistic = "$$\\mathbb{C}v\\{X_t, X_{t-1}\\}$$",

Theoric = sigma^2 * par[2],

Empiric = cov(Xt[-1], lag(Xt,1)[-1])),

tibble(Statistic = "$$\\mathbb{C}r\\{X_t, X_{t-1}\\}$$",

Theoric = par[2]/(1 + par[2]^2),

Empiric = acf_j[1]))

kab %>%

knitr::kable(format = "html", escape = FALSE, booktabs = FALSE, align = 'c') %>%

kableExtra::row_spec(0, color = "white", background = "green") | Statistic | Theoric | Empiric |

|---|---|---|

| $$\mathbb{E}\{X_t\}$$ | 0.0000000 | -0.0157117 |

| $$\mathbb{V}\{X_t\}$$ | 1.0225000 | 1.0937676 |

| $$\mathbb{C}v\{X_t, X_{t-1}\}$$ | 0.1500000 | 0.1412342 |

| $$\mathbb{C}r\{X_t, X_{t-1}\}$$ | 0.1466993 | 0.1290617 |

2 AR(p) process

Let’s consider an autoregressive process of order \(p\), namely \(X_t \sim AR(P)\), i.e. \[ x_t = \mu + \sum_{i=1}^{p}\phi_{i} x_{t-i} + u_{t} \text{,} \] where in general \(u_t \sim \text{MDS}(0, \sigma^2)\).

Let’s consider a process \(X_t \sim AR(1)\), i.e. \[ x_t = \mu + \phi_{1} x_{t-1} + u_{t} \text{.} \] Through recursion up to time 0 it is possible to express an AR(1) model as an MA(\(\infty\)), i.e. \[ X_t = \phi_1^{t} X_0 + \mu \sum_{i=0}^{t-1} \phi_{1}^{i} + \sum_{i = 0}^{t-1} \phi_{1}^{i} u_{t-i} \] where the process is stationary if and only if \(|\phi_1|<1\). In fact, independently from the specific distribution of the residuals \(u_t\), the unconditional expectation of an AR(1) converges if and only if \(|\phi_1|<1\), i.e. \[ \mathbb{E}\{X_t\} = \phi_1^{t} X_0 + \mu \sum_{i=0}^{t-1} \phi_{1}^{i} = \frac{\mu}{1-\phi_1} \]

The variance instead is computed as: \[ \gamma_0 = \mathbb{V}\{X_t\} = \sum_{i=0}^{t-1} \phi_{1}^{2i} \sigma^{2} = \frac{\sigma^{2}}{1-\phi_{1}^2} \] The auto covariance decays exponentially fast depending on the parameter \(\phi_1\), i.e. \[ \begin{aligned} \gamma_1 {} & = \mathbb{C}v\{X_t, X_{t-1}\} = \phi_{1} \frac{\sigma^{2}}{1-\phi_{1}^2} = \phi_1 \gamma_0 \end{aligned} \] and in general: \[ \begin{aligned} \gamma_k {} & = \mathbb{C}v\{X_t, X_{t-k}\} = \phi_{1}^{|k|} \gamma_0 \text{.} \end{aligned} \] Finally, the auto correlation function is given by: \[ \begin{aligned} \rho_{1} {} & = \mathbb{C}r\{X_t, X_{t-1}\} = \\ & = \frac{\mathbb{C}v\{X_t, X_{t-1}\}}{\sqrt{\mathbb{V}\{X_t\} \mathbb{V}\{X_{t-1}\}}} = \\ & = \frac{\gamma_1}{\gamma_0} = \phi_1 \end{aligned} \] and in general: \[ \begin{aligned} \rho_{k} {} & = \mathbb{C}r\{X_t, X_{t-k}\} = \phi_{1}^{|k|} \text{.} \end{aligned} \]

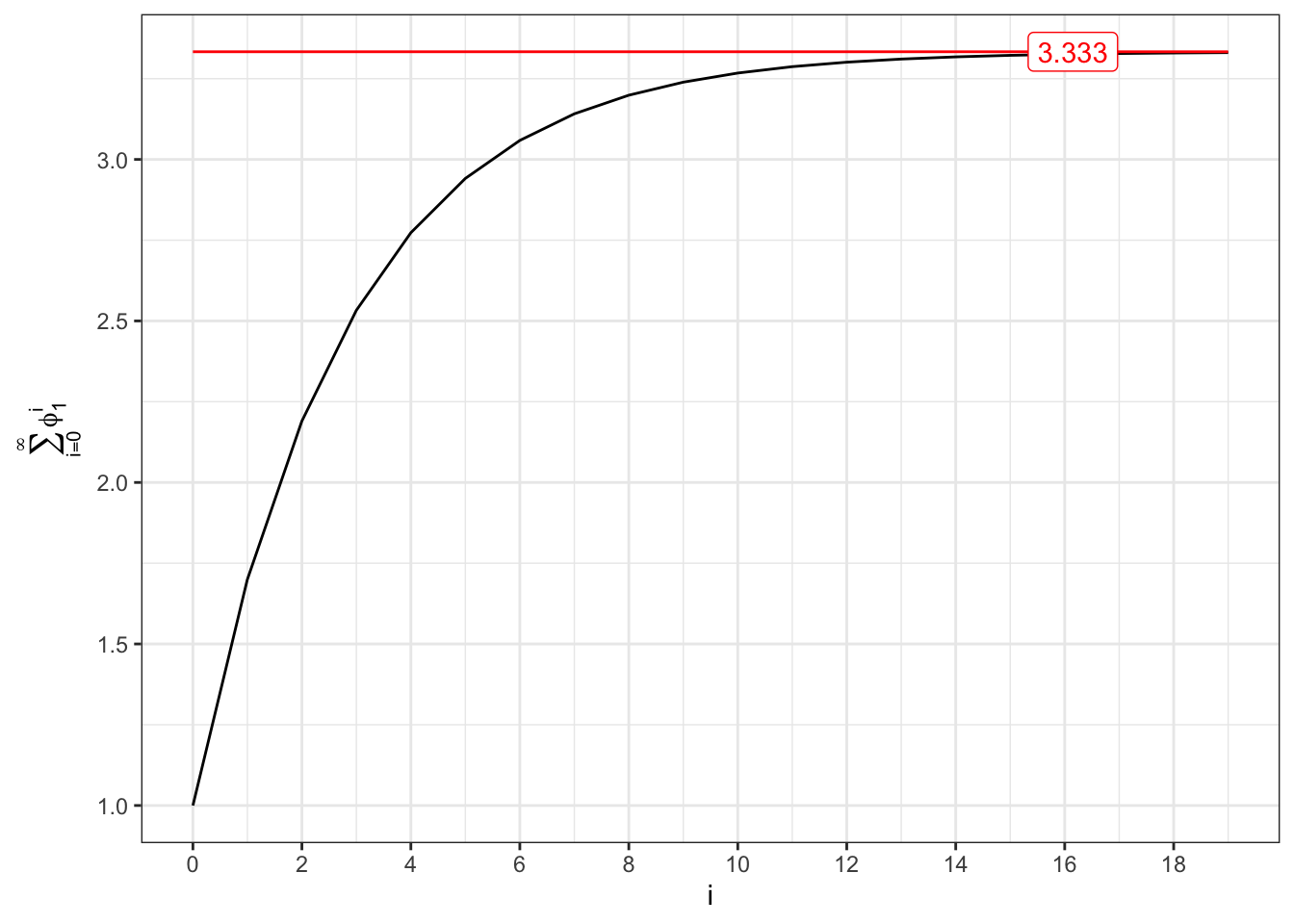

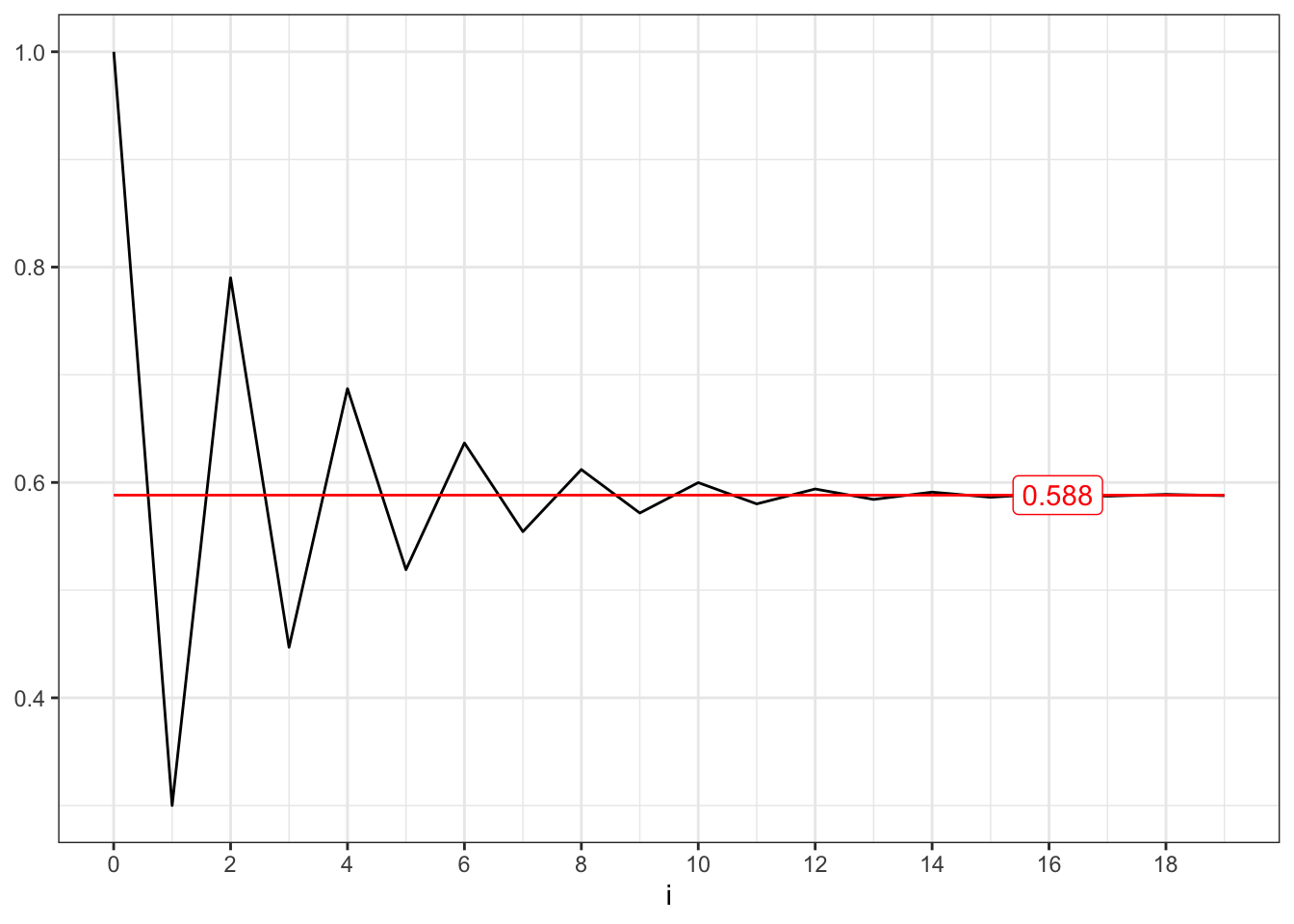

The stationary of an AR(1) process is related to the convergence of two series. The unconditional expectation converges if and only if following series converges, i.e. \[ \sum_{i=0}^{\infty} \phi_1^{i} = \frac{1}{1-\phi_1} \quad\text{iff}\quad |\phi_1| < 1 \text{.} \]

Convergent series (I)

# ==================== Setups =====================

phi <- c(0.7, -0.7)

min_i <- 0

max_i <- 20

i <- seq(min_i, max_i - 1, 1)

y_breaks <- seq(min_i, max_i, 2)

x_labels <- quantile(i, 0.85)

# =================================================

# Convergent series 0 < phi < 1

series1 <- cumsum(phi[1]^i)

limit1 <- 1/(1 - phi[1])

plot_1 <- ggplot()+

geom_line(aes(i, series1))+

geom_line(aes(i, limit1), color = "red")+

geom_label(aes(x_labels, limit1, label = round(limit1, 3)), color = "red")+

labs(x = "i", y = TeX("$\\sum_{i=0}^{\\infty} \\phi_{1}^{i}$"))+

scale_x_continuous(breaks = y_breaks)+

theme_bw()

# Convergent series -1 < phi < 0

series2 <- cumsum(phi[2]^i)

limit2 <- 1/(1 - phi[2])

plot_2 <- ggplot()+

geom_line(aes(i, series2))+

geom_line(aes(i, limit2), color = "red")+

geom_label(aes(x_labels, limit2, label = round(limit2, 3)), color = "red")+

labs(x = "i", y = NULL)+

scale_x_continuous(breaks = y_breaks)+

theme_bw()

plot_1

plot_2

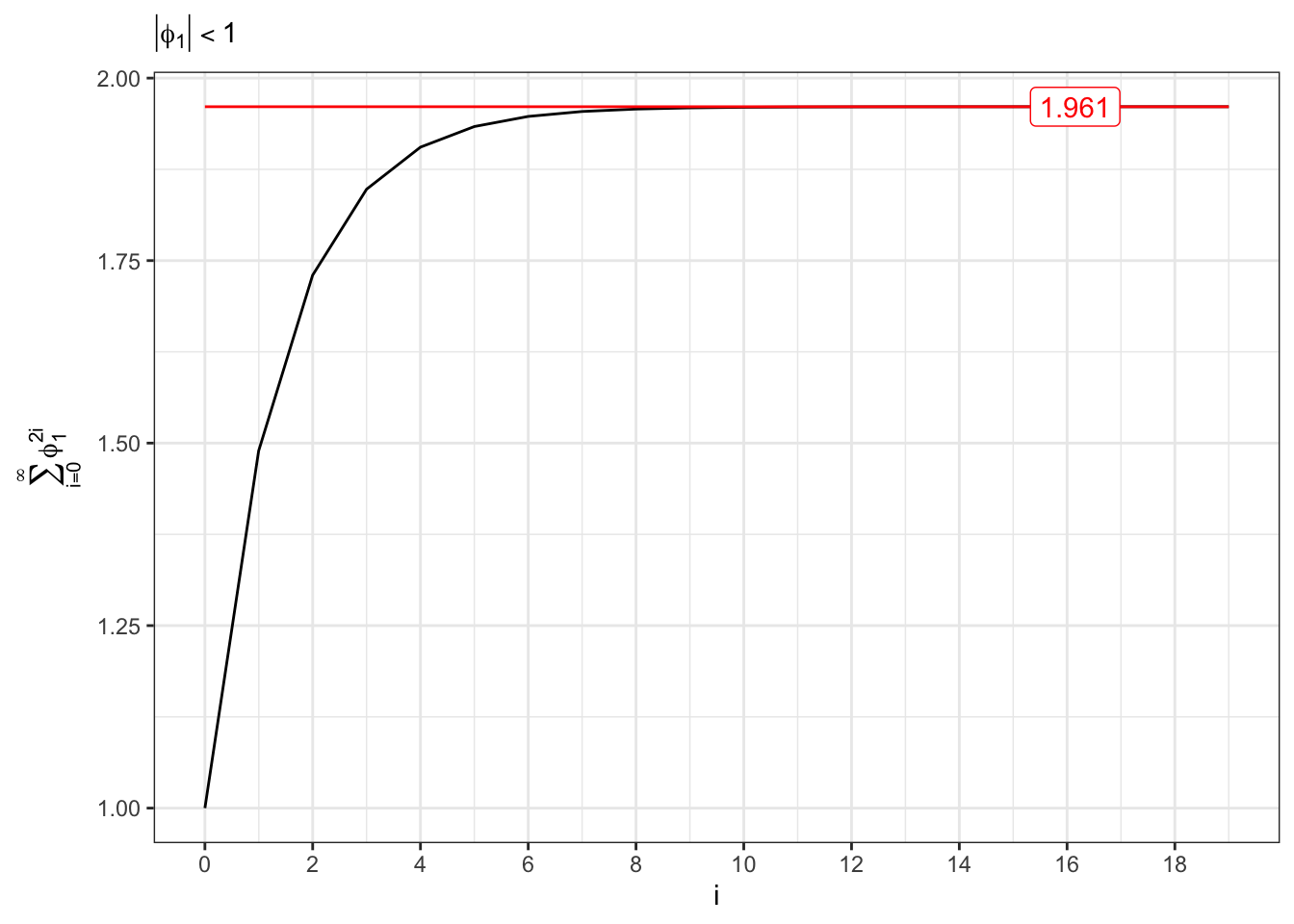

The convergence of the variance is related to the following series, i.e. \[ \sum_{i=0}^{\infty} \phi_1^{2i} = \frac{1}{1-\phi_1^2} \quad\text{iff}\quad |\phi_1| < 1 \text{.} \]

Convergent series (II)

# Convergent series |phi| < 1

series1 <- cumsum(phi[1]^(i*2))

limit1 <- 1/(1 - phi[1]^2)

ggplot()+

geom_line(aes(i, series1))+

geom_line(aes(i, limit1), color = "red")+

geom_label(aes(x_labels, limit1, label = round(limit1, 3)), color = "red")+

labs(x = "i", y = TeX("$\\sum_{i=0}^{\\infty} \\phi_{1}^{2i}$"), subtitle = TeX("$|\\phi_1| < 1$"))+

scale_x_continuous(breaks = y_breaks)+

theme_bw()

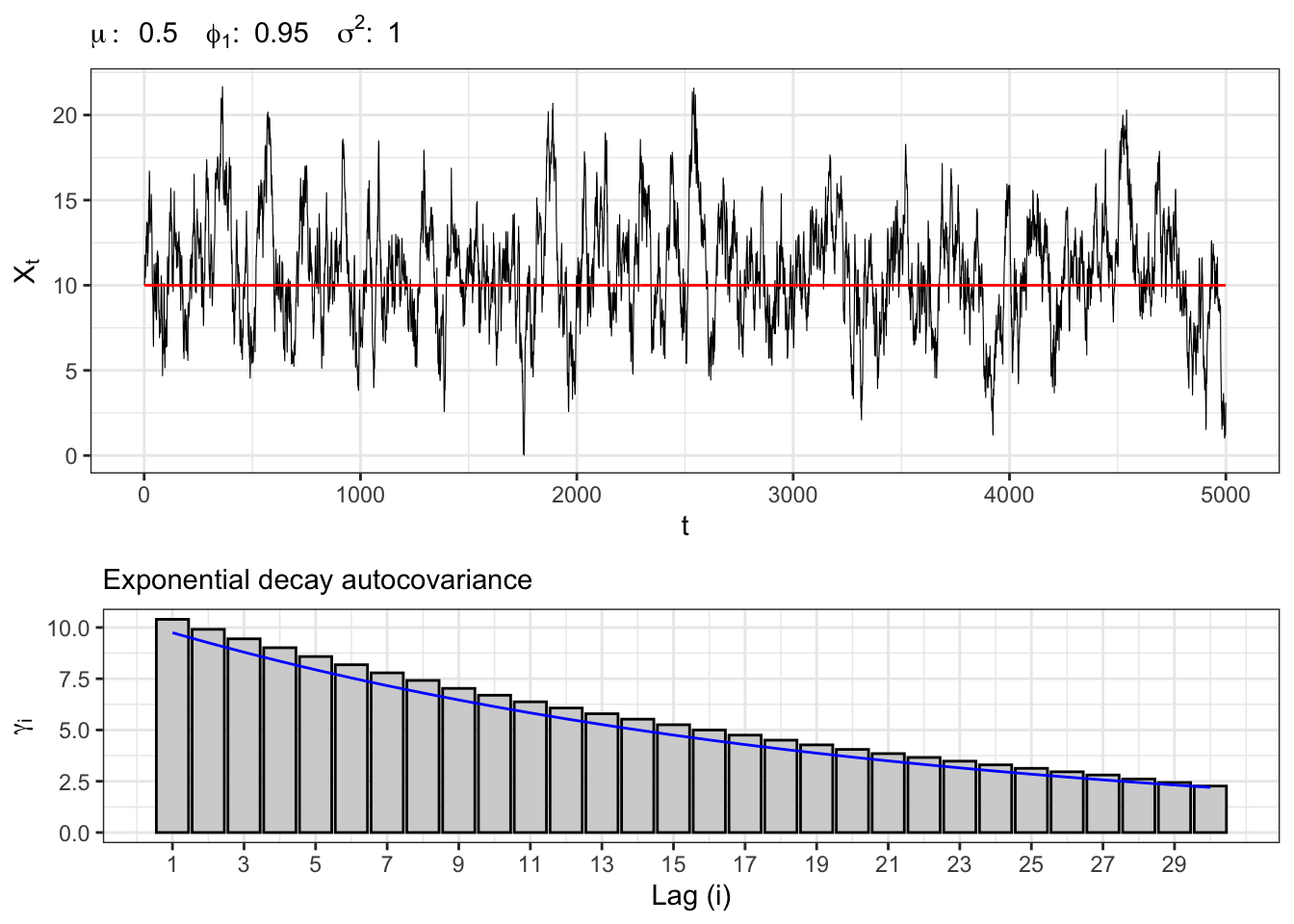

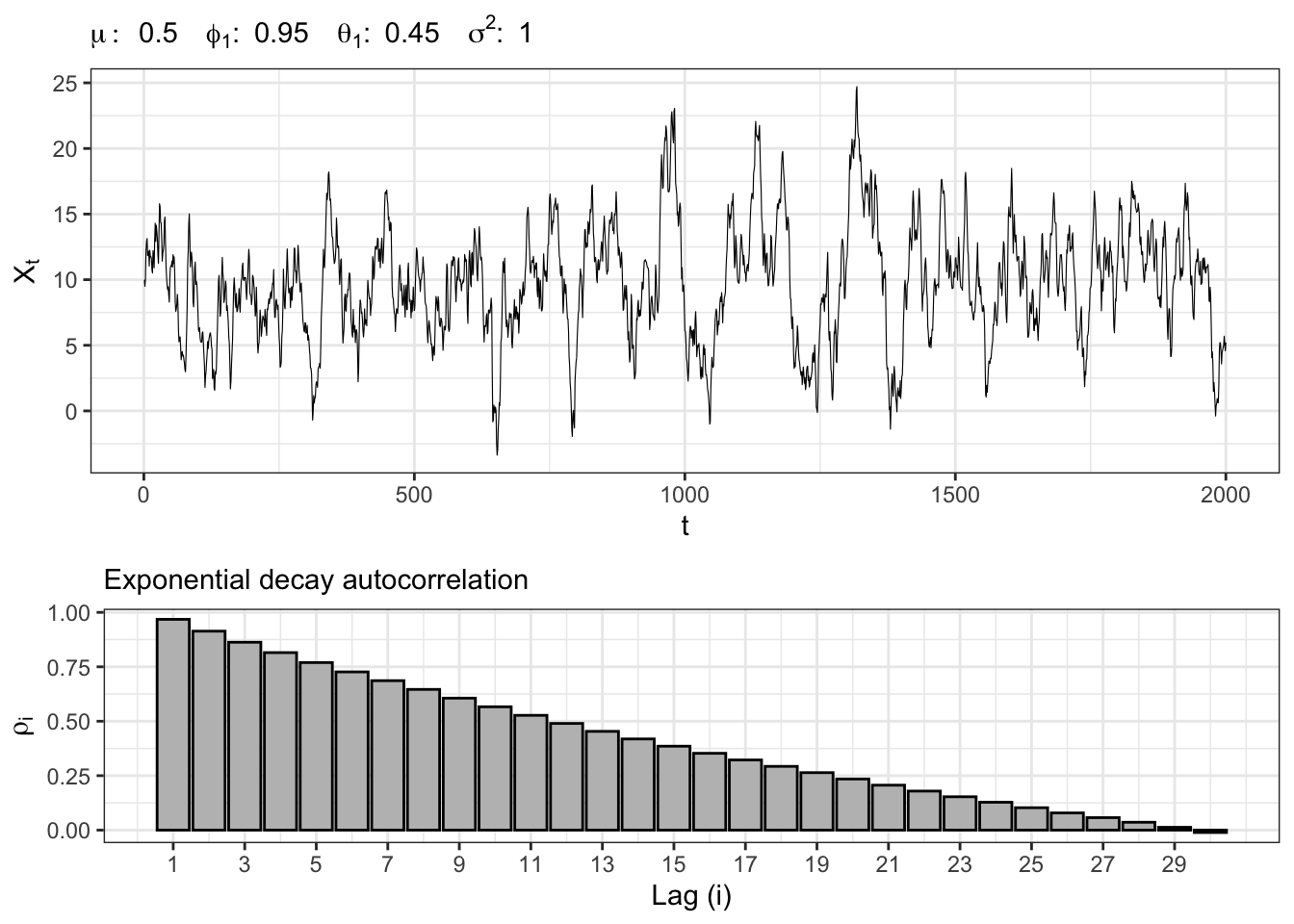

2.1 Example: AR(1)

Let’s simulate an autoregressive Gaussian process, namely \(X_t \sim AR(1)\), i.e. \[ x_t = \mu + \phi_{1} x_{t-1} + u_{t} \text{,} \] where \(u_t \sim \mathcal{N}(0, \sigma^2)\).

AR(1) simulation

# ==================== Setups =====================

set.seed(2) # random seed

t_bar <- 5000 # number of simulations

par <- c(mu = 0.5, phi1 = 0.95) # parameters

sigma <- 1 # sd of epsilon

lag.max <- 30 # maximum lag for acf

Xt <- c(par[1]/(1-par[2])) # initial point

# ================== Simulation ===================

# Simulated residuals

eps <- rnorm(t_bar, mean=0, sd=sigma)

# simulated AR(1)

for(t in 2:t_bar){

Xt[t] <- par[1] + par[2]*Xt[t-1] + eps[t]

}

# ===================== Plot ======================

# AR(1) simulation

plot_ar <- ggplot()+

geom_line(aes(1:t_bar, Xt), size = 0.2)+

geom_line(aes(1:t_bar, par[1]/(1-par[2])), color = "red")+

theme_bw()+

labs(x = "t", y = TeX("$X_t$"),

subtitle = TeX(paste0("$\\mu:\\;", par[1],

"\\;\\; \\phi_{1}:\\;", par[2],

"\\;\\; \\sigma^2 : \\;", sigma^2,

"$")))

# AR(1) autocorrelation

lags <- 1:lag.max

x_breaks <- seq(1, lag.max, 2)

acf_j <- acf(Xt, plot = FALSE, lag.max = lag.max, type = "cov")$acf[,,1][-1]

plot_acf <- ggplot()+

geom_histogram(aes(lags, acf_j), stat = "identity", fill = "lightgray", color = "black")+

geom_line(aes(lags, (par[2]^abs(lags))*(sigma^2)/(1-par[2]^2) ), color = "blue")+

scale_x_continuous(breaks = x_breaks, labels = x_breaks)+

theme_bw() +

labs(x = "Lag (i)", y = TeX("$\\gamma_{i}$"),

subtitle = "Exponential decay autocovariance")

gridExtra::grid.arrange(plot_ar, plot_acf, heights = c(0.6, 0.4))

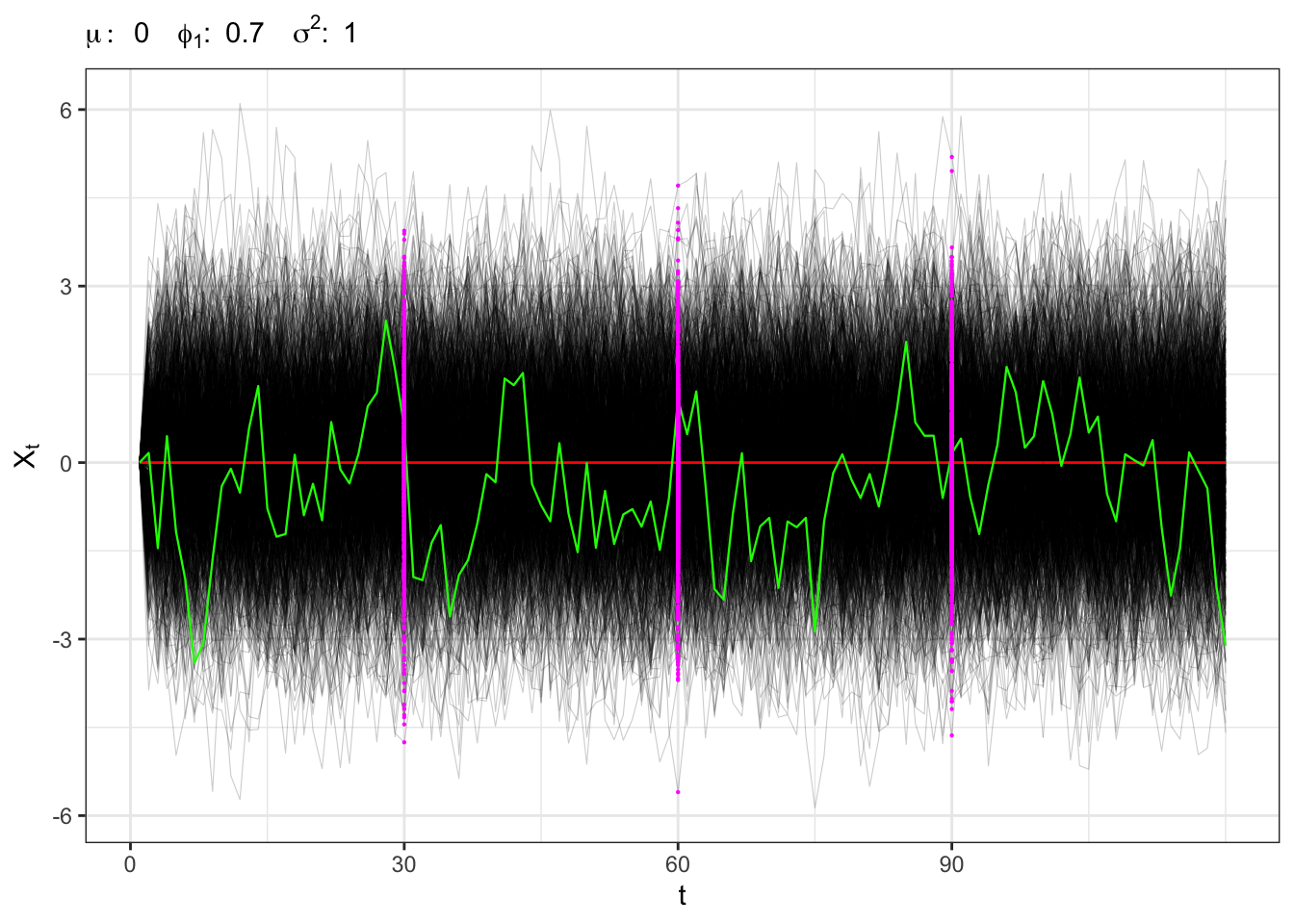

2.2 Example: stationary AR(1)

Stationary AR(1)

# ==================== Setups =====================

set.seed(3) # random seed

t_bar <- 120 # number of steps ahead

j_bar <- 1000 # number of simulations

sigma <- 1 # standard deviation of epsilon

par <- c(mu = 0, phi1 = 0.7) # parameters

X0 <- par[1]/(1-par[2]) # initial point

t_sample <- c(30,60,90) # sample times

# ================== Simulation ===================

# Process Simulations

scenarios <- tibble()

for(j in 1:j_bar){

Xt <- c(X0)

# Simulated residuals

eps <- rnorm(t_bar, 0, sigma)

# Simulated AR(1)

for(t in 2:t_bar){

Xt[t] <- par[1] + par[2]*Xt[t-1] + eps[t]

}

df <- tibble(j = rep(j, t_bar), t = 1:t_bar, Xt = Xt, eps = eps)

scenarios <- bind_rows(scenarios, df)

}

# ===================== Plot ======================

# Trajectory j

df_j <- dplyr::filter(scenarios, j == 6)

# Sample at different times

df_t1 <- dplyr::filter(scenarios, t == t_sample[1])

df_t2 <- dplyr::filter(scenarios, t == t_sample[2])

df_t3 <- dplyr::filter(scenarios, t == t_sample[3])

# Paths plots

ggplot()+

geom_line(data = scenarios, aes(t, Xt, group = j), alpha = 0.2, size = 0.2)+

geom_line(data = df_j, aes(t, par[1]/(1-par[2])), color = "red")+

geom_line(data = df_j, aes(t, Xt), color = "green", size = 0.4)+

geom_point(data = df_t1, aes(t, Xt), color = "magenta", size = 0.1)+

geom_point(data = df_t2, aes(t, Xt), color = "magenta", size = 0.1)+

geom_point(data = df_t3, aes(t, Xt), color = "magenta", size = 0.1)+

scale_x_continuous(breaks = seq(0, 100, 30))+

theme_bw()+

labs(x = "t", y = TeX("$X_t$"),

subtitle = TeX(paste0("$\\mu:\\;", par[1],

"\\;\\; \\phi_{1}:\\;", par[2],

"\\;\\; \\sigma^2 : \\;", sigma^2,

"$")))

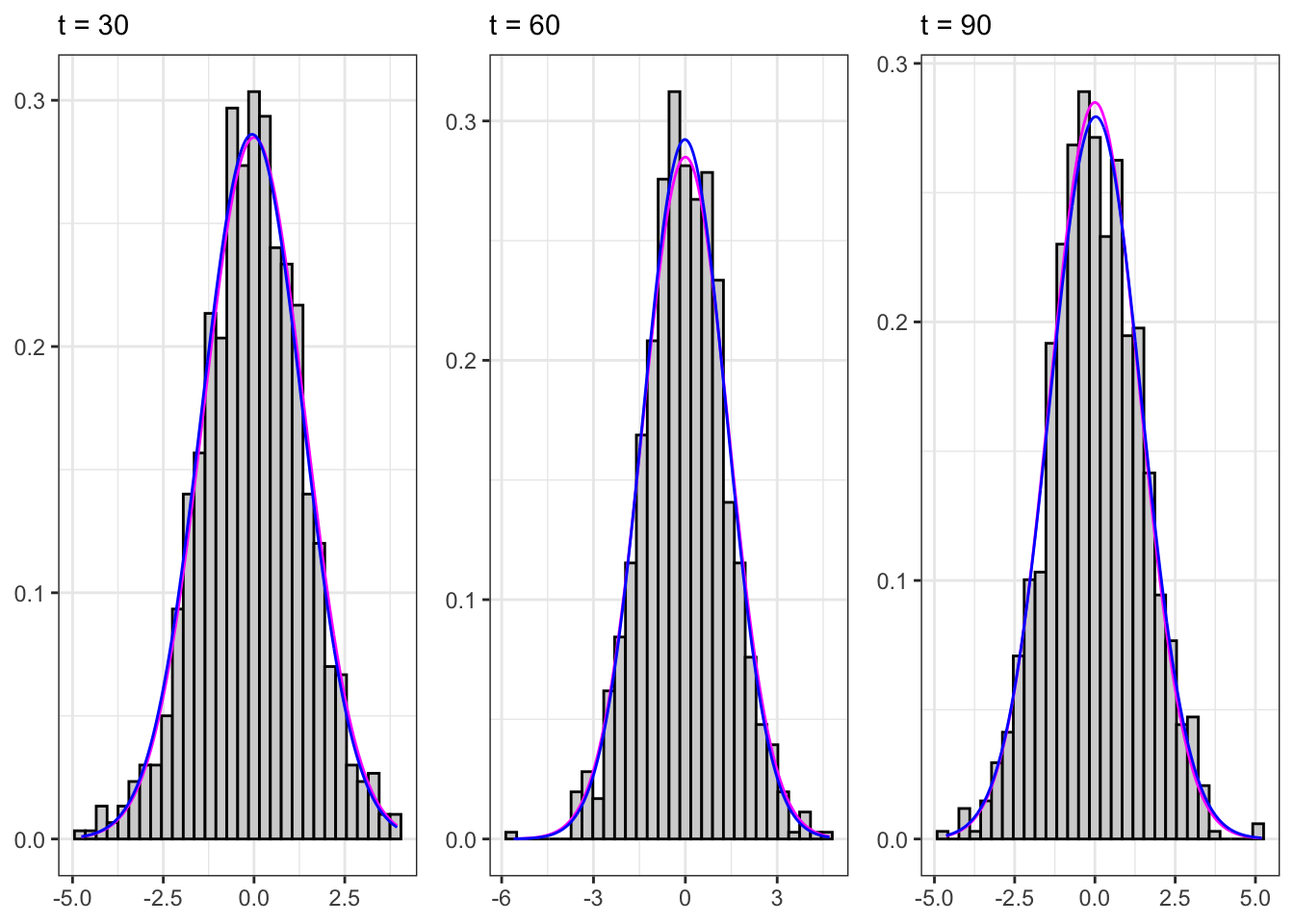

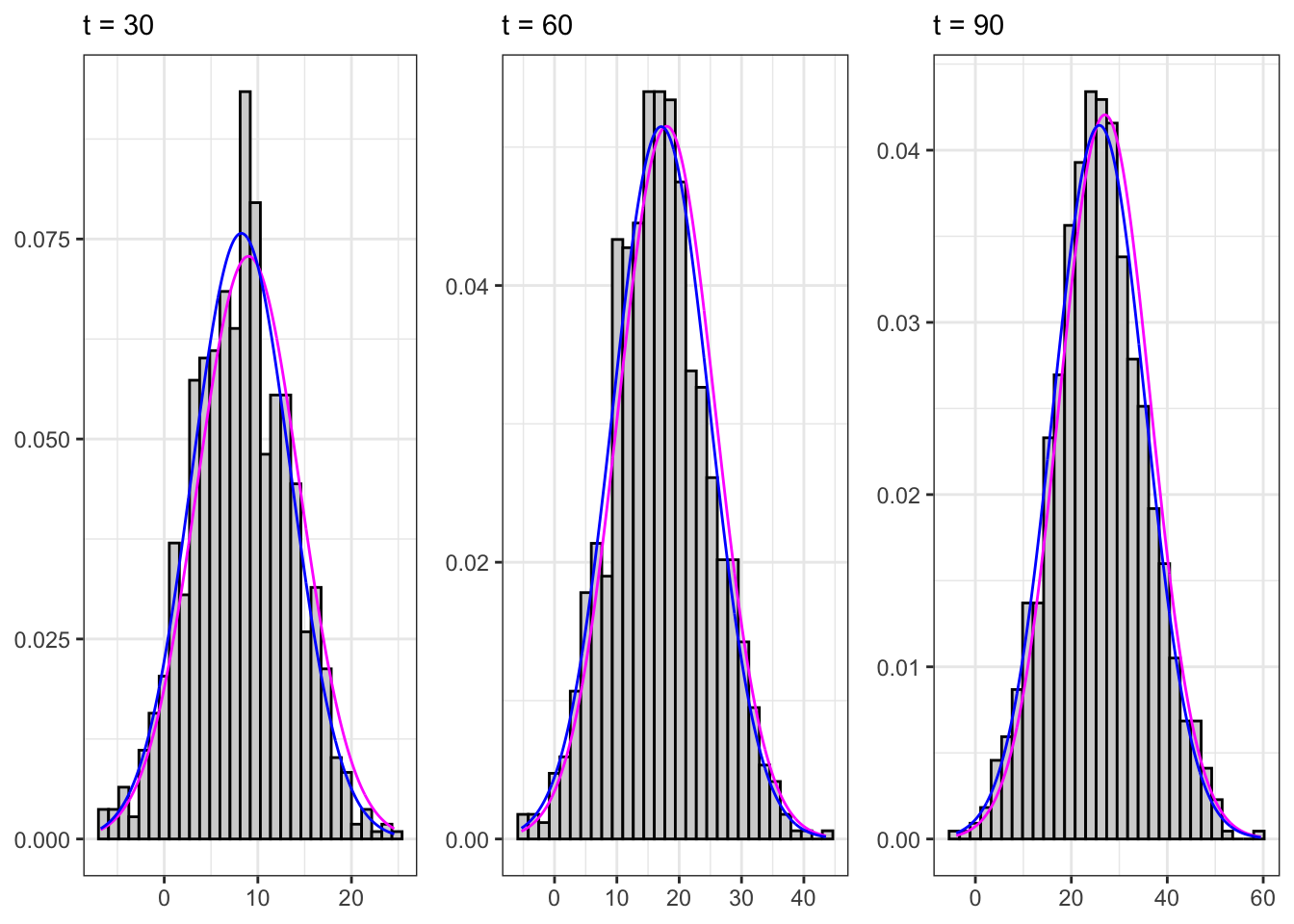

Sampling the process for different \(t\) we expect that, on a large number of simulations, the distribution will be normal with stationary moments, i.e. \[ X_t \sim \mathcal{N}\left(\frac{\mu}{1-\phi_{1}}, \frac{\sigma^{2}}{1-\phi_{1}^2} \right) \forall t \text{.} \]

Sampled AR(1)

# ================== Setups ==================

bins <- 30 # bins for histograms

# Stationary moments

e_x <- par[1]/(1-par[2])

sd_x <- sqrt((sigma^2)/(1 - par[2]^2))

# ================= Sample 1 =================

samp1 <- df_t1

df_grid1 <- list()

# Grid of points

df_grid1$grid <- seq(min(samp1$Xt), max(samp1$Xt), length.out = nrow(samp1))

# Stationary theoric pdf

df_grid1$pdf_theoric <- dnorm(df_grid1$grid, e_x, sd_x)

# Stationary empiric pdf

df_grid1$pdf_empiric <- dnorm(df_grid1$grid, mean(samp1$Xt), sd(samp1$Xt))

df_grid1 <- bind_cols(df_grid1)

plot_t1 <- ggplot()+

geom_histogram(data = samp1, aes(Xt, after_stat(density)),

bins = bins, color = "black", fill = "lightgray")+

geom_line(data = df_grid1, aes(grid, pdf_theoric), color = "magenta")+

geom_line(data = df_grid1, aes(grid, pdf_empiric), color = "blue")+

labs(subtitle = paste0("t = ", samp1$t[1]), x = NULL, y = NULL)+

theme_bw()

# ================= Sample 2 =================

samp2 <- df_t2

df_grid2 <- list()

# Grid of points

df_grid2$grid <- seq(min(samp2$Xt), max(samp2$Xt), length.out = nrow(samp2))

# Stationary theoric pdf

df_grid2$pdf_theoric <- dnorm(df_grid2$grid, e_x, sd_x)

# Stationary empiric pdf

df_grid2$pdf_empiric <- dnorm(df_grid2$grid, mean(samp2$Xt), sd(samp2$Xt))

df_grid2 <- bind_cols(df_grid2)

plot_t2 <- ggplot()+

geom_histogram(data = samp2, aes(Xt, after_stat(density)),

bins = bins, color = "black", fill = "lightgray")+

geom_line(data = df_grid2, aes(grid, pdf_theoric), color = "magenta")+

geom_line(data = df_grid2, aes(grid, pdf_empiric), color = "blue")+

labs(subtitle = paste0("t = ", samp2$t[1]), x = NULL, y = NULL)+

theme_bw()

# ================= Sample 3 =================

samp3 <- df_t3

df_grid3 <- list()

# Grid of points

df_grid3$grid <- seq(min(samp3$Xt), max(samp3$Xt), length.out = nrow(samp3))

# Stationary theoric pdf

df_grid3$pdf_theoric <- dnorm(df_grid3$grid, e_x, sd_x)

# Stationary empiric pdf

df_grid3$pdf_empiric <- dnorm(df_grid3$grid, mean(samp3$Xt), sd(samp3$Xt))

df_grid3 <- bind_cols(df_grid3)

plot_t3 <- ggplot()+

geom_histogram(data = samp3, aes(Xt, after_stat(density)),

bins = bins, color = "black", fill = "lightgray")+

geom_line(data = df_grid3, aes(grid, pdf_theoric), color = "magenta")+

geom_line(data = df_grid3, aes(grid, pdf_empiric), color = "blue")+

labs(subtitle = paste0("t = ", samp3$t[1]), x = NULL, y = NULL)+

theme_bw()

gridExtra::grid.arrange(plot_t1, plot_t2, plot_t3, ncol = 3)

| Statistic | Theoric | Empiric |

|---|---|---|

| $$\mathbb{E}\{X_t\}$$ | 0.000000 | -0.0027287 |

| $$\mathbb{V}\{X_t\}$$ | 1.960784 | 1.9530614 |

| $$\mathbb{C}v\{X_{t}, X_{t-1}\}$$ | 1.372549 | 1.3586670 |

| $$\mathbb{C}r\{X_{t}, X_{t-1}\}$$ | 0.700000 | 0.6956660 |

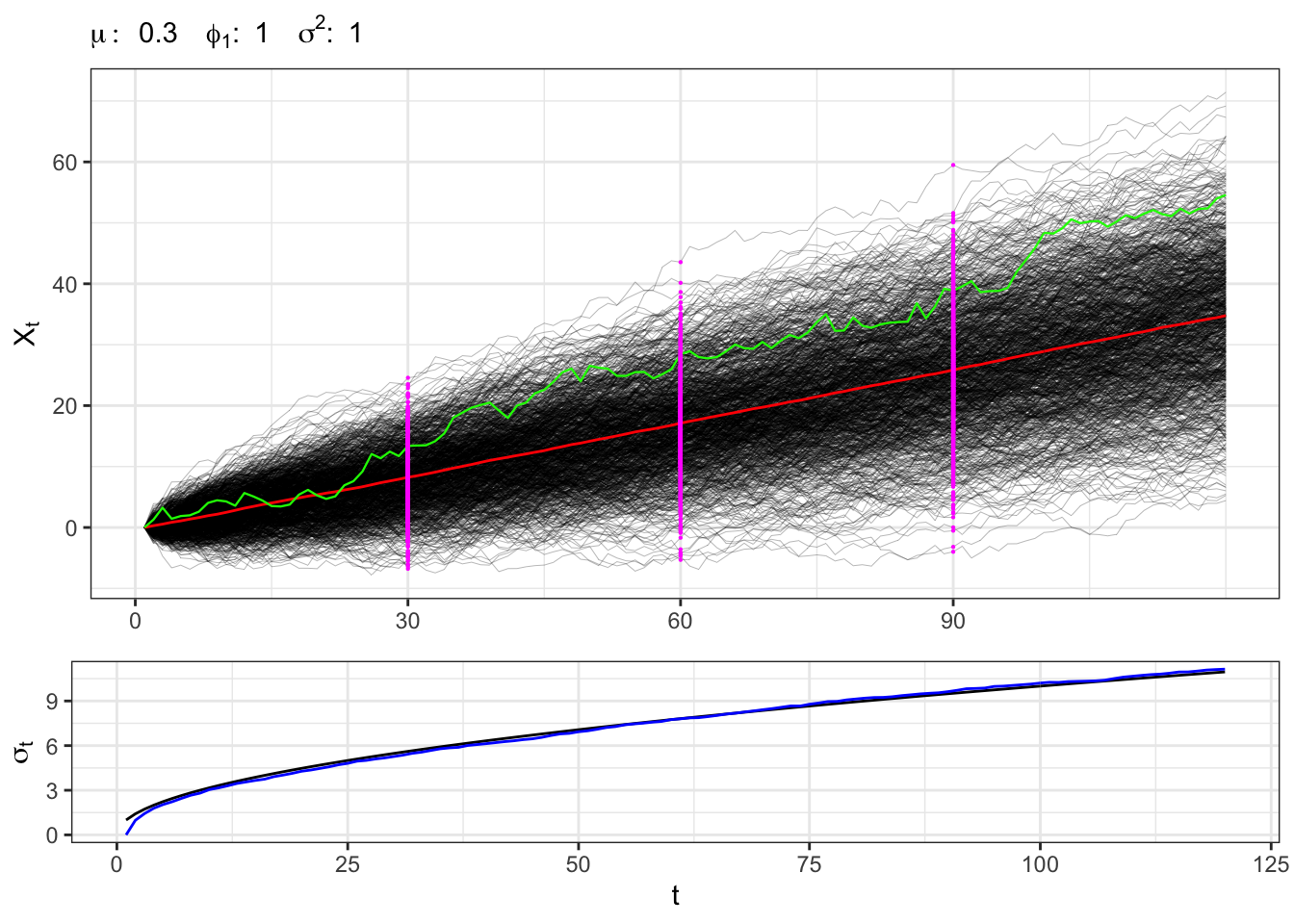

2.3 Example: non-stationary AR(1)

A non-stationary process has \(\phi_1 = 1\), for example let’s consider a random walk with drift, i.e. \[ x_t = \mu + x_{t-1} + u_{t} \text{,} \] or equivalently \[ x_t = X_0 + \mu t + \sum_{i = 0}^{t-1} u_{t-i} \text{.} \] In this setting, the expectation and variance of the process do not converges but tends to explode as \(t\) increases, i.e. \[ \begin{aligned} {} & \mathbb{E}\{X_t\} = X_0 + \mu t \\ & \mathbb{V}\{X_t\} = t \sigma^{2} \end{aligned} \quad\text{iff}\quad \phi_1 = 1 \]

Non-stationary AR(1)

# ==================== Setups =====================

set.seed(5) # random seed

t_bar <- 120 # number of steps ahead

j_bar <- 1000 # number of simulations

sigma0 <- 1 # standard deviation of epsilon

par <- c(mu = 0.3, phi1 = 1) # parameters

X0 <- c(0) # initial point

t_sample <- c(30,60,90) # sample times

# ================== Simulation ===================

# Process Simulations

scenarios <- tibble()

for(j in 1:j_bar){

# Initialize X0 and variance

Xt <- rep(X0, t_bar)

sigma <- rep(sigma0, t_bar)

# Simulated residuals

eps <- rnorm(t_bar, mean=0, sd=sigma0)

for(t in 2:t_bar){

sigma[t] <- sigma0*sqrt(t)

Xt[t] <- par[1] + par[2]*Xt[t-1] + eps[t]

}

df <- tibble(j = rep(j, t_bar), t = 1:t_bar, Xt = Xt,

sigma = sigma, eps = eps)

scenarios <- dplyr::bind_rows(scenarios, df)

}

# Compute simulated moments

scenarios <- scenarios %>%

group_by(t) %>%

mutate(e_x = mean(Xt), sd_x = sd(Xt))

# ===================== Plot ======================

# Trajectory j

df_j <- dplyr::filter(scenarios, j == 6)

# Sample at different times

df_t1 <- dplyr::filter(scenarios, t == t_sample[1])

df_t2 <- dplyr::filter(scenarios, t == t_sample[2])

df_t3 <- dplyr::filter(scenarios, t == t_sample[3])

# Non-stationary paths

plot_paths <- ggplot()+

geom_line(data = scenarios, aes(t, Xt, group = j),

alpha = 0.5, size = 0.1)+

geom_line(data = df_j, aes(t, e_x, group = j), color = "red")+

geom_line(data = df_j, aes(t, Xt), color = "green", size = 0.4)+

geom_point(data = df_t1, aes(t, Xt), color = "magenta", size = 0.1)+

geom_point(data = df_t2, aes(t, Xt), color = "magenta", size = 0.1)+

geom_point(data = df_t3, aes(t, Xt), color = "magenta", size = 0.1)+

scale_x_continuous(breaks = seq(0, 100, 30))+

theme_bw()+

labs(x = NULL, y = TeX("$X_t$"),

subtitle = TeX(paste0("$\\mu:\\;", par[1],

"\\;\\; \\phi_{1}:\\;", par[2],

"\\;\\; \\sigma^2 : \\;", sigma0^2,

"$")))

# Non-stationary std. deviation

plot_sigma <- ggplot(df_j)+

geom_line(aes(t, sigma, group = j), alpha = 1)+

geom_line(aes(t, sd_x, group = j), alpha = 1, color = "blue")+

labs(x = "t", y = TeX("$\\sigma_{t}$"))+

theme_bw()

gridExtra::grid.arrange(plot_paths, plot_sigma, heights = c(0.7, 0.3))

Sampling the process for different \(t\) we expect that, on a large number of simulations, the distribution will be normal with non-stationary moments, i.e. \[ X_t \sim \mathcal{N}\left(\mu t, \sigma^{2} t \right) \text{.} \]

Sampled non-stationary AR(1)

# ================== Setups ==================

bins <- 30 # bins for histograms

# ================= Sample 1 =================

samp1 <- df_t1

df_grid1 <- list()

# Grid of points

df_grid1$grid <- seq(min(samp1$Xt), max(samp1$Xt), length.out = nrow(samp1))

# Non stationary theoric pdf

df_grid1$pdf_theoric <- dnorm(df_grid1$grid, X0 + par[1]*samp1$t[1], samp1$sigma[1])

# Non stationary empiric pdf

df_grid1$pdf_empiric <- dnorm(df_grid1$grid, samp1$e_x[1], samp1$sd_x[1])

df_grid1 <- bind_cols(df_grid1)

plot_t1 <- ggplot()+

geom_histogram(data = samp1, aes(Xt, after_stat(density)),

bins = bins, color = "black", fill = "lightgray")+

geom_line(data = df_grid1, aes(grid, pdf_theoric), color = "magenta")+

geom_line(data = df_grid1, aes(grid, pdf_empiric), color = "blue")+

labs(subtitle = paste0("t = ", samp1$t[1]), x = NULL, y = NULL)+

theme_bw()

# ================= Sample 2 =================

samp2 <- df_t2

df_grid2 <- list()

# Grid of points

df_grid2$grid <- seq(min(samp2$Xt), max(samp2$Xt), length.out = nrow(samp2))

# Non stationary theoric pdf

df_grid2$pdf_theoric <- dnorm(df_grid2$grid, X0 + par[1]*samp2$t[1], samp2$sigma[1])

# Non stationary empiric pdf

df_grid2$pdf_empiric <- dnorm(df_grid2$grid, samp2$e_x[1], samp2$sd_x[1])

df_grid2 <- bind_cols(df_grid2)

plot_t2 <- ggplot()+

geom_histogram(data = samp2, aes(Xt, after_stat(density)),

bins = bins, color = "black", fill = "lightgray")+

geom_line(data = df_grid2, aes(grid, pdf_theoric), color = "magenta")+

geom_line(data = df_grid2, aes(grid, pdf_empiric), color = "blue")+

labs(subtitle = paste0("t = ", samp2$t[1]), x = NULL, y = NULL)+

theme_bw()

# ================= Sample 3 =================

samp3 <- df_t3

df_grid3 <- list()

# Grid of points

df_grid3$grid <- seq(min(samp3$Xt), max(samp3$Xt), length.out = nrow(samp3))

# Non stationary theoric pdf

df_grid3$pdf_theoric <- dnorm(df_grid3$grid, X0 + par[1]*samp3$t[1], samp3$sigma[1])

# Non stationary empiric pdf

df_grid3$pdf_empiric <- dnorm(df_grid3$grid, samp3$e_x[1], samp3$sd_x[1])

df_grid3 <- bind_cols(df_grid3)

plot_t3 <- ggplot()+

geom_histogram(data = samp3, aes(Xt, after_stat(density)),

bins = bins, color = "black", fill = "lightgray")+

geom_line(data = df_grid3, aes(grid, pdf_theoric), color = "magenta")+

geom_line(data = df_grid3, aes(grid, pdf_empiric), color = "blue")+

labs(subtitle = paste0("t = ", samp3$t[1]), x = NULL, y = NULL)+

theme_bw()

gridExtra::grid.arrange(plot_t1, plot_t2, plot_t3, ncol = 3)

3 ARMA(p,q) process

An ARMA(p,q) process is a combination of an MA(q) and an AR(p) processes, i.e. an \(X_t \sim ARMA(p,q)\) is defined as \[ x_t = \mu + \sum_{i=1}^{p}\phi_{i} x_{t-i} + \sum_{j=1}^{q}\theta_{j} u_{t-j} + u_{t} \text{,} \] where in general \(u_t \sim \text{MDS}(0, \sigma^2)\).

3.1 Example: ARMA(1,1)

Let’s simulate a Gaussian autoregressive moving-average process, namely \(X_t \sim ARMA(1,1)\), i.e. \[ x_t = \mu + \phi_{1} x_{t-1} + \theta_{1} u_{t-1} + u_{t} \text{,} \] where \(u_t \sim \mathcal{N}(0, \sigma^2)\).

ARMA(1,1) simulation

# ======================== Setups ========================

set.seed(6) # random seed

t_bar <- 2000 # Number of steps ahead

# Parameters

par <- c(mu = 0.5, phi1 = 0.95, theta1 = 0.45)

sigma <- 1 # Standard deviation of epsilon

lag.max <- 30 # Maximum lag for acf

# ===================== Simulations =====================

# Initial value

Xt <- c(par[1]/(1-par[2]))

# Simulated residuals

eps <- rnorm(t_bar, 0, sigma)

# Simulated ARMA(1,1)

for(t in 2:t_bar){

Xt[t] <- par[1] + par[2]*Xt[t-1] + par[3]*eps[t-1] + eps[t]

}

# ======================== Plot =========================

# ARMA(1,1) simulation

plot_arma <- ggplot()+

geom_line(aes(1:t_bar, Xt), size = 0.2)+

theme_bw()+

labs(x = "t", y = TeX("$X_t$"),

subtitle = TeX(paste0("$\\mu:\\;", par[1],

"\\;\\; \\phi_{1}:\\;", par[2],

"\\;\\; \\theta_{1}:\\;", par[3],

"\\;\\; \\sigma^2 : \\;", sigma^2,

"$")))

# ARMA(1,1) autocorrelation

lags <- 1:lag.max

y_breaks <- seq(1, lag.max, 2)

acf_j <- acf(Xt, plot = FALSE, lag.max = lag.max, type = "cor")$acf[,,1][-1]

plot_acf <- ggplot()+

geom_histogram(aes(lags, acf_j), stat = "identity", fill = "gray", color = "black")+

scale_x_continuous(breaks = y_breaks)+

theme_bw()+

labs(x = "Lag (i)", y = TeX("$\\rho_{i}$"),

subtitle = "Exponential decay autocorrelation")

gridExtra::grid.arrange(plot_arma, plot_acf, heights = c(0.6, 0.4))

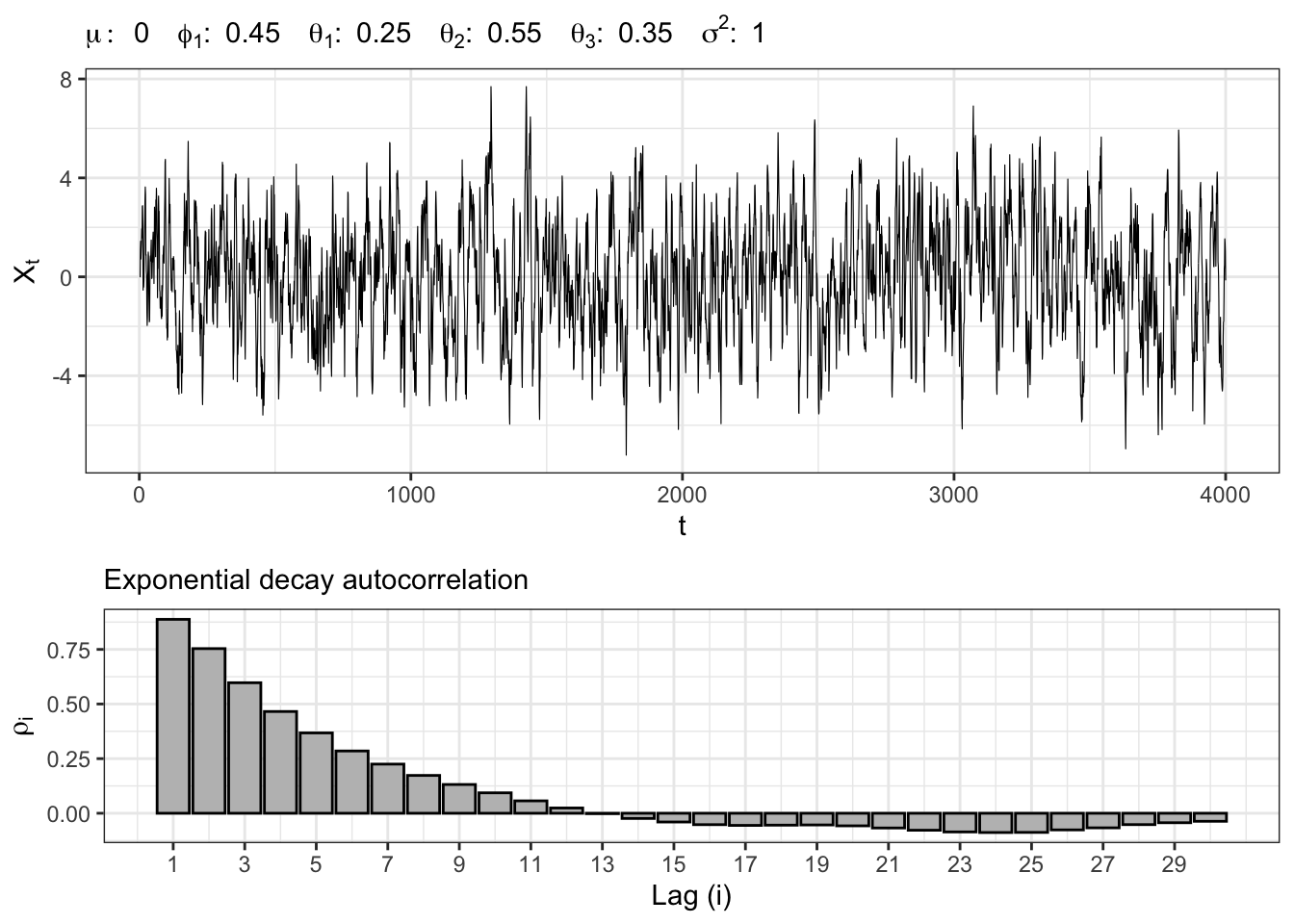

3.2 Example: ARMA(2,3)

Let’s simulate another Gaussian autoregressive moving-average process, namely \(X_t \sim ARMA(2,3)\), i.e. \[ x_t = \mu + \sum_{i = 1}^{2} \phi_{i} x_{t-i} + \sum_{j = 1}^{3} \theta_{j} u_{t-j} + u_{t} \text{,} \] where \(u_t \sim \mathcal{N}(0, \sigma^2)\).

ARMA(2,3) simulation

# ======================== Setups ========================

set.seed(7) # random seed

t_bar <- 4000 # Number of steps ahead

# Parameters

par <- c(mu = 0, phi1 = 0.45, phi2 = 0.25,

theta1 = 0.55, theta1 = 0.35, theta1 = 0.15)

sigma <- 1 # Standard deviation of epsilon

lag.max <- 30 # Maximum lag for acf

# ===================== Simulations =====================

# Random seed

set.seed(1)

# Initial value

Xt <- rep(0, 4)

# Simulated ARMA(1,1)

eps <- rnorm(t_bar, 0, sigma)

for(t in 4:t_bar){

# AR component

Xt[t] <- par[1] + par[2]*Xt[t-1] + par[3]*Xt[t-2]

# MA component

Xt[t] <- Xt[t] + par[4]*eps[t-1] + par[5]*eps[t-2] + par[6]*eps[t-3] + eps[t]

}

# ======================== Plot =========================

# ARMA(1,1) simulation

plot_arma <- ggplot()+

geom_line(aes(1:t_bar, Xt), size = 0.2)+

theme_bw()+

labs(x = "t", y = TeX("$X_t$"),

subtitle = TeX(paste0("$\\mu:\\;", par[1],

"\\;\\; \\phi_{1}:\\;", par[2],

"\\;\\; \\theta_{1}:\\;", par[3],

"\\;\\; \\theta_{2}:\\;", par[4],

"\\;\\; \\theta_{3}:\\;", par[5],

"\\;\\; \\sigma^2 : \\;", sigma^2,

"$")))

# ARMA(1,1) autocorrelation

lags <- 1:lag.max

y_breaks <- seq(1, lag.max, 2)

acf_j <- acf(Xt, plot = FALSE, lag.max = lag.max, type = "cor")$acf[,,1][-1]

plot_acf <- ggplot()+

geom_histogram(aes(lags, acf_j), stat = "identity", fill = "gray", color = "black")+

scale_x_continuous(breaks = y_breaks)+

theme_bw()+

labs(x = "Lag (i)", y = TeX("$\\rho_{i}$"),

subtitle = "Exponential decay autocorrelation")

gridExtra::grid.arrange(plot_arma, plot_acf, heights = c(0.6, 0.4))

Citation

@online{sartini2024,

author = {Sartini, Beniamino},

title = {ARMA Process},

date = {2024-05-01},

url = {https://greenfin.it/statistics/arma-models.html},

langid = {en}

}